Win some, lose some, right?

Well, I lost this one. I purchased Amazon stock in September 2020, when it was trading for $155 per share. Like a lot of things in the investing world, it was all going swimmingly until 2022. In fact, as recently as 5th April, it was trading at $168, good for a 8% increase since my purchase. As I write this, however, it’s trading at $122 following a plunge over the last two months.

The reasons are easy to place, and you’re likely sick of hearing about them. The Russian war, the dirty combination of rampant inflation and slowing growth, with all this mixed in with a hawkish Fed. Everything that could go wrong is going wrong, with the result the most risk-off environment in recent environment.

But with a stock-split occurring yesterday, for the first time since the dot-com boom, I felt like re-assessing the stock. Does Amazon now represent a buy, down 25% so far this year and 35% off all-time-highs?

I believe so.

Market Dominance

Amazon has the market cornered. Over half of e-commerce flows through Amazon, an absolutely staggering number. Most people are familiar with that, however the dominance of Amazon Web Services (AWS) is less well-known. AWS commands 33% of the cloud computing market. Indeed, one of the big criticisms of the so-called decentralisation of Web3 is that a vast majority of the platforms are still built on AWS, which is very much centralised.

Cloud computing is a high-growth area that isn’t slowing down. AWS made $18.5 billion in operating profit last year, and over half the entire company’s profit has been drawn from AWS every year since 2014. Its stellar growth is part of the reason that Andy Jassy, head of AWS for 15 years, was selected to succeed Jeff Bezos as CEO.

Furthermore, with odds of an impending recession increasing, this could actually play further into the hands of AWS, as companies will be pushed to jump across to public cloud services rather than constructing their own data centres, which are typically hugely expensive undertakings.

Investment

I have utmost confidence in the AWS side of the business because nothing really needs to change. It has grown at a 35% rate, so even a decline to 15% or 20% would still render it a hugely profitable side of the business. The crux comes on the e-commerce side, where analysts have been getting increasingly bearish.

But things are not as dire as the market would lead you to believe here, either. In fact, Amazon has been here before. It recently reported its first quarterly loss at $3.8 billion since 2015 and warned that further losses may be ahead. Shares promptly slipped 10%.

But this was largely due to the distribution infrastructure which the company doubled in two years, having taken over two decades to build up the original infrastructure. Notably, this is exactly what happened in the dot-com boom, when Amazon also reported operating losses in the billions while investing heavily in itself.

Just like it did then, Amazon is sacrificing current profits for future ones. It’s a tale as old as time. If Amazon were a private company, investors would be pleased. But ugly quarterly earnings and the thirst for immediate gratification are pulling down the share price.

Valuation

You don’t need to listen to me rambling on about AWS and e-commerce. Amazon’s strengths are well publicised. But what has changed over the last month is the valuation. It now trades at an enterprise value-to-EBITDA ratio of 18.9, compared to an average of over 52 since 2008.

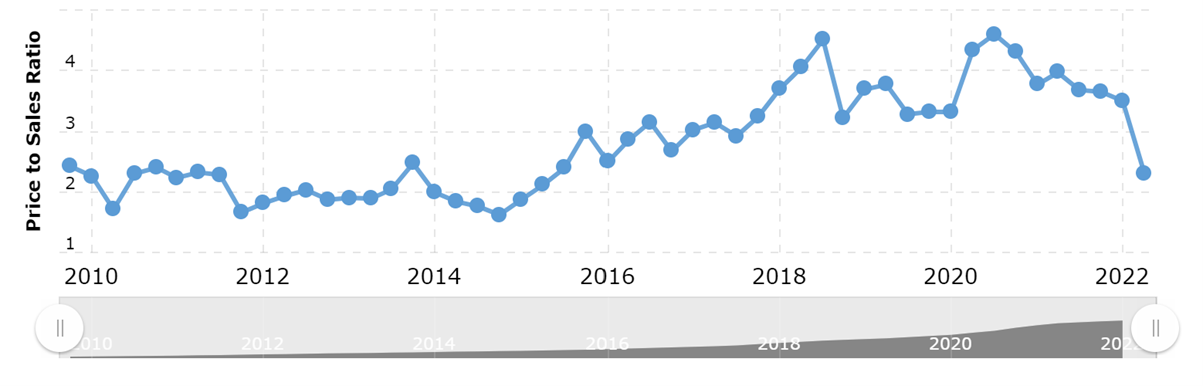

The price-to-sales ratio also looks cheap at 2.31, down to its lowest value since 2015, as the below graph shows.

The board was also permitted to repurchase $10 billon of stock in March, a move which looked to take advantage of declining valuations. The normal caveat of share repurchases suggesting faltering growth does not apply here – Amazon has historically been very reluctant to buy back and has already spent hugely in recent times, as discussed above. There is no shortage of growth and innovation plans here – e-commerce, cloud computing, digital advertising, Prime video (sports expansion) all have big plans, to name a few.

Conclusion

In summary, nothing really has changed for Amazon. The market right now is obviously abhorrent, with prices slashed across every asset class. I’m not sure the cut taken out of Amazon is justified, however.

Its cloud computing business (AWS) remains a juggernaut, with growth unlikely to cease anytime soon. The e-commerce side has drawn gasps from analysts, but I’m more than willing to place my faith in management that the heightened expenditure over the last two years will bear fruit in the future – especially given we have seen this from Amazon in the past.

With the AWS cushion to fall back on, Amazon will be just fine. Throw in the discount valuation metrics and what I view as a promising move to buy back stock, and Amazon looks like good value – the best value we have seen in a while.

I don’t really see anything worse right now with the company as a prospect, compared to my thesis in buying it in 2020. Sure, I’m underwater on the purchase after a market meltdown and maybe this is just an expressive form of coping, but selling my Amazon stock here has not even crossed my mind.